Break Even Point

Cost is an important aspect to be taken care of in economics as well as Cost. Every business aims to lower or cut its costs and increase profits.

In economics and cost accounting, break-even point refers to the point where the total revenue of the business is equal to the total cost of the business. This is the point where the business is said to be breaking even its cost i.e. no profit no loss. It is the lowest point in the business where it survives. If its total revenues fall any further, the business will not be able to cover its costs and hence it will have to shut down its business. Break-even point serves as the bottom line.

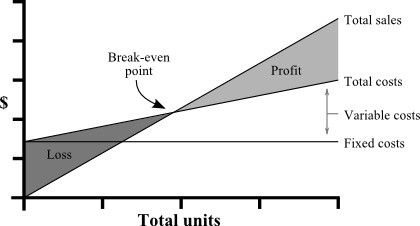

Break Even Point is where Total Cost = Total Revenue i.e. TC = TR

From the given figure we can clearly understand that the point where the Total Cost’s line intersects with the Total Revenue’s line; it is the point where both are equal and forms the Break- Even point. Here the company neither earns any profit nor incurs any loss.

How is the Break-even Analysis useful?

The Break Even Analysis is a very useful method in the business management. It helps in determining the level of sales a business needs to make to cover its cost i.e. reach a situation where it is neither in losses nor earning profits. The sales for break-even point can be calculated in units as well as the total amount.

This break-even analysis works great as a means of planning the business’s future endeavors and deciding what level of pricing or sales it should do. This is a great tool for planning the functions. It forms the basis for the marketing department as they can set a goal for the sales in the business. They will make every effort to achieve that benchmark of sales to break even the cost.

Further, it is helpful to the business management too. The business management gets an insight into the situation of the business and it can take steps to cut down the costs of the business so that the business starts to earn profits. This will help the business to achieve cost leadership and increase optimum utilization of resources.

Break-even analysis is a widely used tool for the new growing startups and entrepreneurial plans. Break-even analysis helps them to apply formulae to their business models and check if their business model is competitive and has the potential to survive the market forces.

The Break-even Analysis can be used in different manners to draw results regarding different components. Break-even analysis can be used for finding many other results such as:

-

Break-even (in sales) = It refers to the number of sales the business needs to make so that the Cost becomes equal to revenues. In other words, break even can be defined as Sale Price of the good = Cost price of the good (after taking into the fixed cost in consideration).

Break-even Point (In sales amount) =Fixed cost/p/vRatio

Where, P/V Ratio =Contribution/Sales ×100

-

Break-even (in quantity) = Break- Even analysis is used to calculate the units required to be sold to arrive at the Break-even point.

Break- Even Point (In quantity) =(Total Fixed Cost)/(Contribution per unit)

-

The margin of Safety: Margin of Safety can be defined the strength of the business enterprise to operate above the break-even point. In other words, it is the number of sales beyond the level of Break-Even Point. It is where the business enjoys the safety of operations as it no longer has to worry about meeting its cost. This point shows that the business is earning profits.

Margin of safety = Current Output – Output at the Breakeven Point

-

The margin of safety Percentage: It is the percentage of the margin of safety of the company in comparison to its break-even point.

Margin of Safety % =(Current Output - Break Even Output)/(Current Output)×100

Analysis of Break-even Point: The Break-even point is affected by three components: Variable Cost, Fixed Cost, and Sales Volume. The Break-even point will behave differently to every change in these three elements. These are the three major determinants in determining the break-even point of the company. The variable cost is the cost that fluctuates with the number of products to be manufactured and the fixed cost always remains stable i.e. does not change.

The following example can be used to calculate Break-even point and related concepts:

| Particular | Amount |

|---|---|

| Sales | $10000 |

| Fixed Cost | 1000 |

| Variable Cost | $5 |

| Sales(units) | 1000 |

| Total variable Cost (Variable Cost*Sales Unit) | $5000 |

| Contribution (Sales-Total Variable Cost) | $5000 ($10000-$5000) |

P/V Ratio= Contribution/Sales ×100

= 5000/10000×100

= 50%

Break-even point (in sales) = (Fixed Cost)/(P/V Ratio)

= 1000/(50%)

$2000

Break- even point (in quantity) = (Total Fixed Cost)/(Contribution per unit)

= 1000/5

= 200 units

Margin of Safety = Current Output – Output at the Breakeven Point

=1000 – 200 units

= 800 units

Margin of Safety Percentage = (Current Output - Break Even Output)/(Current Output)×100

= (1000-200)/1000×100

= 80%

Limitations of Break-Even Point Analysis:

-

Break-even analysis is only cost oriented. It does not take into consideration the Sales effects or what they actually should be by taking into consideration the prices of the products. It is a simple method yet due to its drawbacks it is not widely used.

-

Break-even analysis is only applicable to the enterprise’s short run costing. IT assumes fixed costs to be fixed i.e. stable. Whereas in case of long-term, the costs are always variable.

-

The assumption of the average variable cost being equal for all the products is highly unlikely. Sometimes the variable cost may vary from product to product.

-

It does not take into consideration the products lying unsold with the enterprise i.e. inventory with the enterprise. These goods are not sold yet and should be accounted for. Break-even point’s assumption that the goods produced are equal to the goods sold is highly unlikely.

-

The assumption of constant sales mix is highly irrelevant.

How can urgenthomework.com help you in making Accounting Assignments?

Urgenthomework.com has a team of experts who excel in their respective fields and have vast knowledge in their fields. We have created this team over the years with best knowledge and expertise. These experts will help you in writing excellent and authentic content for your assignment which will help you score well. You can also take doubts from our experts or can opt for Online tutoring on various subjects like Management, Mathematics, and English etc. These coaching will help you in boosting your confidence and scoring good marks in the subjects you desire. So what are you waiting for? Just post your query with our customer executive or you can talk to them through live chat.

You can submit your assignment online with a deadline and ask our customer executive for a quote. Make the payment and get your assignment delivered on time.