Detective controls – will not prevent errors from occurring but rather they alert those using the system to error and anomalies

StuDocu is not sponsored or endorsed by any college or university

ACCG 2 5 0 : ACCO U N TI N G SYSTEM S D ESI G N & D EV EL O PM EN T

Today Every Company is a Technology Company

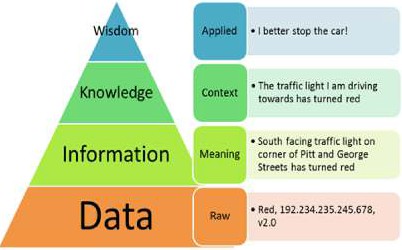

Definitions

|

|

|---|---|

Why should I learn about IS?

Reason 1: Benefits of becoming and informed user

BENEFITS OF BECOMING AN INFORMED USER:

Benefit from organisation’s IT application – you can understand what is behind those applications

Can play a key role in managing the organisation’s IS

Can use IT to start your own business

Reason 2: IT offers Career Opportunities

Business Analyst

Systems Programmer

Reason 3: IT/Information can offer a Competitive Advantage

Overview of Computer-Based Systems

Computer-based Information

Systems

Computer-based Information

Systems

Hardware – devices accept, process and display data and info

Software – program(s) enable hardware to process data

Major Capabilities of Information Systems

Performs speedy, high-volume calculations

Provide fast, communication

and collaboration among organisations

Provide fast, communication

and collaboration among organisations

Types of Organisational Information Systems Evolution of AIS

How Does IT Impact Organisations?

IT Reduces the Number of Middle Managers

IT makes managers more productive more people report to one manager Reduces number of middle managers (Fewer promotional opportunities)

IT Changes the Manager’s Job

Will IT Eliminate Jobs?

HOWEVER

IT creates new jobs that requires employees with IT knowledge and skills, e.g. medical record keeping

IT Impacts Employees at Work

|

Ergonomics: science of designing machines and work settings that minimise injury and illness

Importance of Information Systems to Society

IT affects the quality of our life. Here are the positive and negative, societal effects of the increased use of IT:

Business Processes

Business Process = INPUTS + RESOURCES + OUTPUTS

Effective (customer satisfied) and Efficient (less wastage of resources) Business Processes Competitive Advantage

Information Systems & Business Processes

Allows easy exchange of and access to data across processes

IS plays a vital role in 3 areas:

|

|

BP Improvement, BP Reengineering & BP Management

Business Process Reengineering

Popularity grew due to unique capabilities of IT, e.g. automation of process steps

Business Process Improvement

Five basic phases of BPI:

CONTROL – establishes process metrics and monitors the improved process after solution is implemented

SIX SIGMA (Popular methodology for BPI Initiatives)

Six Sigma: goal is to ensure that the process has no more than 3.4 defects per million outputs

|

|||

|---|---|---|---|

|

|||

BPM Decreases costs Increases revenue Improve Org. Flexibility

Business Pressures, Organisational Responses & IT Support

MARKET PRESSURES

Powerful Customers (customers can use the Internet to learn about p/s)

TECHNOLOGY PRESSURES

Technological innovation & obsolescence (e.g. BYOD)

Information overload

Compliance with government regulations

Ethical issues

Organisations are responding to various business pressures by implementing IT such as:

STRATEGIC SYSTEMS helps increase market share, better negotiate with suppliers, prevent new competitors

Competitive Advantage & Strategic IS

Information Systems + Managing Business Processes Efficiently Competitive Advantage

∆ Competitive advantage is essential for your organisation’s survival

∆ Becoming knowledgeable about strategy and how IS can affect strategy and competitive position will help you throughout your career

Porter’s Five Forces Model

Threat of new entrants – new organisations entering an industry create increased competition for the existing participants

Using the 5 forces model, an organisation can analyse its industry to identify opportunities and threats and then develop tactic for these situations.

Porter’s Value Chain Model

Outbound Logistics – delivering finished product to a customer, invoicing, order handling, finishing goods

Marketing and Sales – promotion of product, sales analysis, market research

Product and technology development (R&D) – product and process design production engineering

Procurement and technology – finding vendors, negotiating prices, new techniques and methods Value system: all value chains (supplier’s value chain, business’ value chain, distributor’s value chain) – firm must understand all components of the value system

Strategies for Competitive Advantage

Operational effectiveness – I can do the same thing more efficiently than you can (improving the manner in which a firm executes its internal business processes to perform these activities more effectively than rivals)

Customer-oriented – I treat my customers better than you do

Business-IT Alignment

6 Characteristics of Excellent Business-IT Alignment

Organizations ensure that IT employees understand how the company makes (or loses) money

Organizations create a vibrant and inclusive company culture

Solution: Adopt process perspective of the organisation

Functional Perspective of an Organisation

Functional perspective: one person doing one task, each department on its own

Process Perspective of an Organisation

Process perspective: all departments must communicate to proceed with all stages of the business process

|

|

|---|---|

|

Functional Perspective vs. Process Perspective

TPS helps prevent errors such as overlapping updates and can be used to reverse transactions.

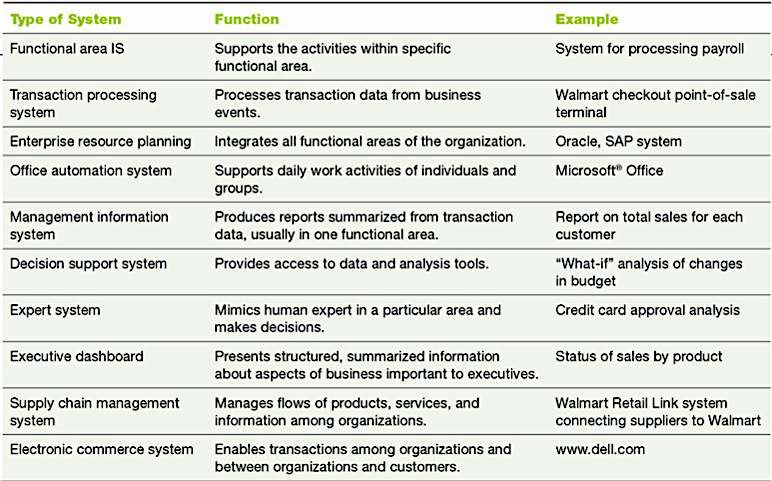

Functional Area Information Systems

A functional area information system supports a functional area by increasing the area’s internal efficiency and effectiveness. Activities supported by FAIS include:

|

|

|

|

Enterprise Resource Planning (ERP) Systems

Historically Functional Area IS developed independently information silos lack of communication & integration

|

|

ERP systems will help an organisation improve its process design when:

The existing process is flawed and the strategy of the organisation is consistent with the ERP approach.

Gather and document current business processes integrate all processes and find the best way of performing those processes, i.e. best practice

Benefits & Limitations of ERP Systems

x Failure to involve affected employees into planning & development phases

x Trying to do too much too fast in conversion process

Implementing ERP Systems

Vanilla approach – implement standard ERP package with little adaptation to org’s business processes

Custom approach – customised ERP system by developing new ERP functions designed specifically for that firm

SOFTWARE-AS-A-SERVICE IMPLEMENTATION

Disadvantages: not necessarily more secure than on-premise systems, companies have a lack of control over system, problems with the system are fixed by the vendor and therefore are not fixed quickly enough

ENTERPRISE APPLICATION INTEGRATION

Used in place of ERP when process of converting from existing system is considered too tiring.

What can go wrong?

Delay in the receipts of products or a delay in a shipment

The system tracks all of the events that occur within each process

The system stores all the documents created in a centralised database that is readily available when needed

Reports

Exception reports – include only information that falls outside certain thresholds (management creates performance standards and then identifies exceptions to this performance standard), e.g. report that shows sales that fell short of the set quota

CHAPTER 4: CUSTOMER RELATIONSHIP MANAGEMENT & SUPPLY CHAIN MANAGEMENT

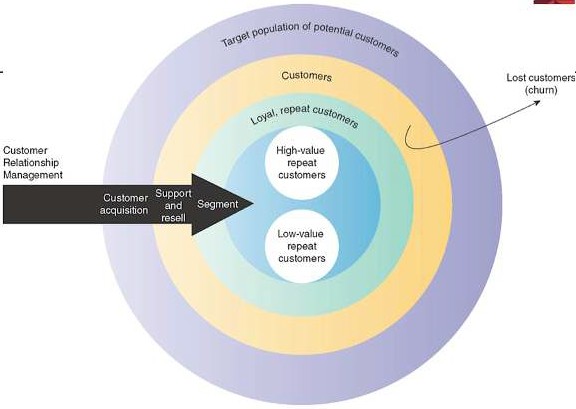

Defining Customer Relationship Management

CRM helps build a long term, sustainable relationship with customers that brings value to the org

Organisational Goal: to maximise number of high-value repeat customers and minimise customer churn Minor increase in customer satisfaction major increase in company’s overall value

Customer Touch Points

Customer Touch Points

Traditional customer touch points – telephone contact, direct mailings, actual physical interactions

Organisational CRM has created new touch points – email, websites, communication via smartphones

Data Consolidation

Operational Customer Relationship Management Systems

A 360-degree view of each customer

The ability of sales and service employee to access a complete history of customer interaction with the organisation, regardless of the touch point

Two Major Components

Contact management system (list of all contacts with customers)

Sales lead tracking system (list of potential customers)

Marketing – CRM applications can sift through customer data – data mining – to develop purchasing profile

Cross Selling – marketing additional related products to customers, e.g. selling camera and showing accessories

Search and Comparison Capabilities

Technical and Other Information and Services, e.g. websites with downloadable product manuals

Customised Products and Services

Personalised Web Pages

FAQs

Analytical Customer Relationship Management Systems

Other types of Customer Relationship Management Systems

On-Demand CRM Systems

∆ Hosted by external vendor in the vendor’s data centre, organisations rent CRM systems from vendors

∆ Pros – Cheaper, less effort, quicker

Mobile CRM Systems

Open Source CRM Systems

∆ Pros – favourable pricing, easy to customise

∆ Cons – risks involving quality control

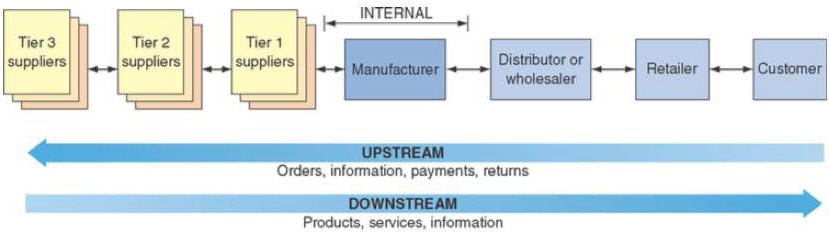

Supply Chains

Structure and Components of Supply Chains

Select suppliers, develop pricing, delivery, payment processes between company and suppliers

Internal – processes

Managers coordinate receipt of orders, develop network of data warehouses, select carrier to deliver products and develop invoicing systems to receive payments from customers

Supply Chain Management

Five Basic Components of Supply Chain Management

DELIVER (Logistics) – Managers coordinate receipt of orders, develop network of data warehouses, select carrier to deliver products and develop invoicing systems to receive payments from customers

RETURN – SC managers must create flexible network for receiving defective, returned or excess products from their customers

Compress the cycle time involves in fulfilling business transactions

Eliminate paper processing and its associated inefficiencies and costs

The Push Model vs. the Pull Model

PULL MODEL (make-to-order) – companies make only what the customer wants

Closely aligned with mass customisation, e.g. Dell laptops

Problems along the Supply Chain

|

|

||

|---|---|---|---|

Solutions to Supply Chain Problems

Information Sharing – along the supply chain

Vendor-managed inventory – when supplier manages the entire inventory process for product(s)

Information technology Support for Supply Chain Management

Definition Internal Control

Why Internal Control systems?

Provides reasonable assurance

Reliability of financial reporting

Internal Control Systems

Internal Control System Objectives

Safeguard assets

Check accuracy and reliability of accounting data

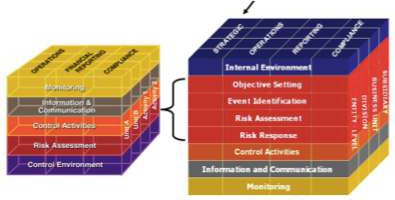

COSO Internal Control – Integrated Framework

COSO Cube 1992 – What makes up Internal Control

Control environment

It is all about top management. If management is asking you to do things that should not be done, then there is no hope for the organisation because it is always top management that makes the big decisions about the firm.

∆ Method of organizing and developing employees

Risk Assessment

Control Activities

» Policies and procedures to protect company assets based on risk assessment e.g. CCTV, gates that beep

To follow the path of data recorded in transaction from the initial source document to final disposition of data on a report or from the report back to the source document

Purpose of Audit Trail

Some controls:

Vacations can be good to uncover fraud while the fraudulent employee is away

SEPARATION OF DUTIES

Good internal controls demand that no single employee be given too much responsibility. An employee should never be in a position to perpetrate and conceal fraud and unintentional errors.

Inventory Controls

Stored in a safe location with limited access, e.g. locks

Use fireproof safes or rented storage vaults offsite

Cash control

Good audit trail of cash disbursements is essential to avoid errors or irregularities

REVIEWS OF OPERATING PERFORMANCE

Duties of Internal Auditors

Operational audits of each department or subsystem in the organisation

Regular reviews of internal control systems

Inform employees about controls

Managers must inform employees about their roles and responsibilities in regards to the control systems

Initiate corrective action when necessary Monitor to see if these controls are effective

2004 COSO

ERM (Enterprise Risk Management) Framework

2004 COSO

ERM (Enterprise Risk Management) Framework

Modified version of COSO cube that includes 3 other components – total of nine.

Objective Setting

Risks tied to what we want to achieve. What are some of the risks around what we want to achieve?, e.g. we want zero injuries in the month, what are some of the risks that will not allow us to achieve this objective

Operations – day-to-day efficiency, performance, and profitability

Event identification & Risk Response

∆ Analyze risks

∆ Implement cost-effective countermeasures

2012 COBIT, Version 5

Meet stakeholders needs

Cover enterprise end-to-end

Identify the source of risks

Determine the impact of risks

Types of Controls

Preventive Controls – are designed to stop errors or irregularities from occurring

Preventing errors and fraud is far more cost-effective than detecting and correcting problems after they occur

IT access authorizations to ensure access is appropriate

The use of passwords to stop unauthorised access to systems/applications

Detective Controls – will not prevent errors from occurring but rather they alert those using the system to error and anomalies

Review your payroll receipts

Compare transactions on reports to source documents

Corrective Controls – designed to correct an error or irregularity after it has occurred

Submit corrective journal entries after discovering an error

Complete changes to IT access lists if individual’s roles changes

Evaluating Controls

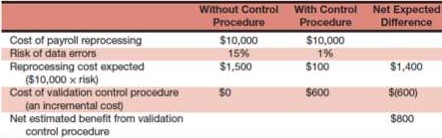

Cost Benefit Analysis

Only the controls whose benefits > costs are implemented. Another alternative is to measure the expected annual loss:

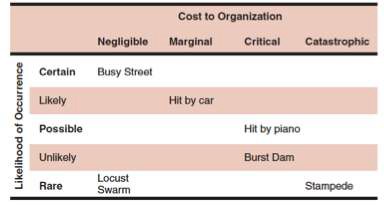

Risk Matrix

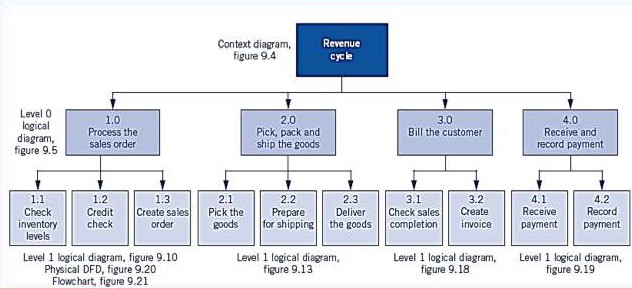

TOPIC 5: REVENUE CYCLE

Strategic Implications of the Revenue Cycle

WHY IS THE REVENUE CYCLE SO IMPORTANT?

The level of sales drives all other activity levels within the organisation

Retail sell product to customer, record sale, collect cash, update inventory

Manufacturer/distributor sell product to other companies, deliver goods, bill customers at a later date, collect payment

Revenue Process Activities (revenue cycle steps)

|

|

|

|

|

|||

|

|

|

10 Source Documents

∆ Credit application – form prepared by new customer applying for credit, shows they financial position

∆ Sales order – formal document prepared using customer order form, multiple copies made for shipment and payments received by customers

∆ Remittance advice – shows cash receipt from customer, outlines nature of payment by customer to accounting or finance unit

∆ Customer service log – used by customer service personnel to record customer enquiries and actions taken to address customer concerns

Technologies Underpinning the Revenue Cycle

CRM (Customer Relationship Management) – improves understanding of customers and their interaction with the organisation (store historical revenue data arranged by customer data mining, trend analysis)

Barcode scanning – reduces error levels by automating data input, scanned data immediately uploaded

Data and Decisions in the Revenue Cycle

Accounts Receivable data (details of payments received, invoices created, cash receipts data)

Sales data (contains details of each sale made)

|

|

Revenue Cycle

Documentation

Revenue Cycle

Documentation

|

||||

|---|---|---|---|---|

|

||||

|

||||

|

|

|||

|

||||

|

||||

|

||||

|

|

|||

|

|

|

||

|

||||

|

||||

|

|

Hash totals: a total that is similar to a batch total but the number that is added has no meaning by itself, e.g. a hash total of customer numbers

5.6 Measuring Revenue Cycle Performance

How to make sure the revenue cycle is achieving its set objectives. To monitor performance a range of metrics need to be employed along with some realistic targets.

Purchasing Phase – Objective is to procure the right goods at the right amount and to receive those goods at the right time

Do this by ensuring approved and authorised purchases, getting goods from authorised suppliers, recording all purchase commitments accurately, accepting goods that meet quality and delivery specification

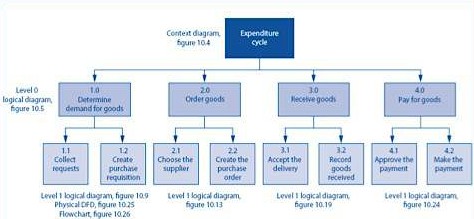

Strategic Implications of the Expenditure Cycle

A well controlled expenditure cycle can provide a competitive advantage by acting to contain costs or by providing high quality products and services which in turn translates to an opportunity for higher product pricing

Failure to correctly manage purchasing can lead to systematic problems that impact revenue and production

Expenditure Process Activities

Source Documents

∆ Vendor List – list of authorised vendors that offer quality goods and services at reasonable prices (part of organisational database)

∆ Purchase Invoice – details and amounts due and payment terms and conditions (prepared by vendor)

Technologies Underpinning the Expenditure Cycle

ERP (Enterprise Resource Planning) – integrated software that records and manages many different types of transactions within a single integrated database, e.g. SAP, Oracle

Improves the integration of enterprise-wide data

EDI is a system or method for exchanging business documents (integrating data from documents into internal systems) with external entities

Without EDI – lost revenue, lost reputation, lost opportunities

E.g. RFID tags used to keep track of pets and livestock (cattle)

SCM (Supply Chain Management) – Improves the planning and execution of orders through supplier and customer integration and detailed supply chain analytics

Data and Decisions in the Expenditure Cycle

|

|

Expenditure Cycle Documentation

Expenditure Cycle DocumentationExpenditure Cycle Activities & Related Risks and Controls

|

|

|

||

|

|

|||

|

|

|

||

|

||||

|

|

|||

|

||||

|

|

|||

|

||||

|

||||

|

|

|||

|

|

|||

|

Measuring Expenditure Cycle Performance

A range of metrics (measure used for a specific purpose) are used to monitor performance against expenditure cycle objectives. Examples of metrics or KPIs for the expenditure cycle objectives include:

|

|

|

|

|

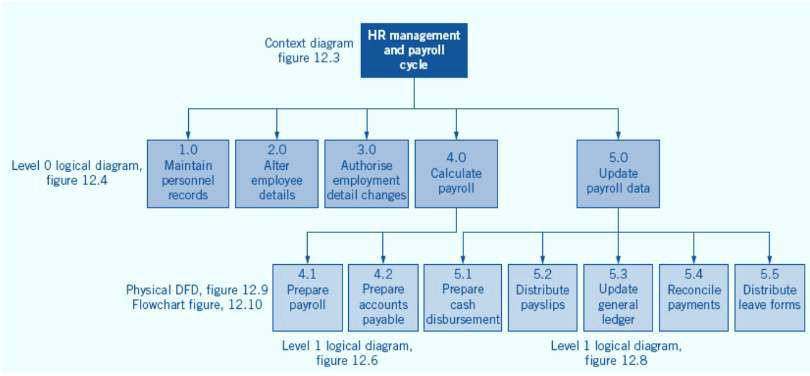

TOPIC 7: HR MANAGEMENT & PAYROLL CYCLE

HR Management Phase – employee recruitment, performance management, management of employee termination

Objective: recruit right people, ensure they are performing at the right standard and manage staff exits in the right manner

Strategic Implications of the HR Management & Payroll Cycle

In order to survive, organisations must not only attract high-performing individuals, but also retain their services for as long as required

HR Management & Payroll Cycle Process Activities (EPPE)

Source Documents

∆ Termination letter – states the terms (date, payout, etc.) of termination of employment

∆ Employee performance review – employers use this form to review an employee’s job performance

Technologies Underpinning the HR Management & Payroll Cycle

Links relevant areas of the organisation, e.g. revenue, production and general ledger

Integrates enterprise-wide data

Online banking facilities improve transparent and reconciliation of transactions – less cash handling

Data and the HR Management & Payroll Cycle

A range of data produced and consumed by activities within the HR management and payroll cycle.

Job vacancies

Current period production cycle data

Accounts payable data

HR Management & Payroll Cycle Business Decisions

|

HR Management & Payroll Cycle

Documentation

HR Management & Payroll Cycle

Documentation

|

||||

|---|---|---|---|---|

|

||||

|

|

|||

|

||||

|

||||

|

|

|

|

|

|

|

|||

|

||||

|

||||

|

||||

|

|

|||

|

|

8.6 Measuring HR Management & Payroll Cycle Performance

Strategies for Acquiring IT Applications

Number of stages may vary but often includes five main stages with the specified tasks and deliverables in each

The stages are to be completed sequentially, one after the other in a linear progression

Alternative Methods and Tools for Systems Development

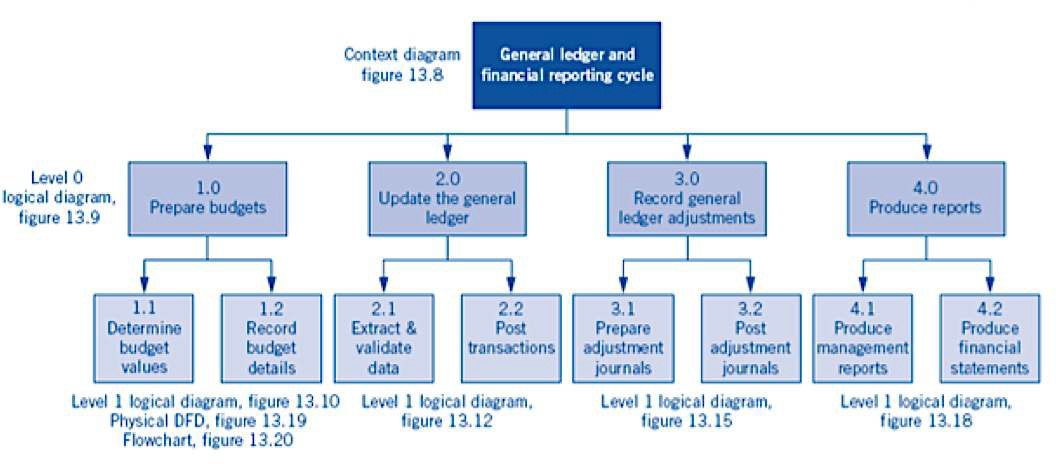

General Ledger & Financial Reporting Cycle Overview & Key Objectives

Finalised budgets are used as a control measure to help ascertain and monitor desirable behaviour by managers within the organisation

Variance analysis: budget estimates compared to actual results (must identify root cause of variance)

Strategic Implications of the General Ledger & Financial Reporting Cycle

Poorly arranged reported data misleading to users

Therefore high quality decision-making requires good data and comprehensible reports.

|

||

|---|---|---|

|

||

|

||

|

||

|

Technologies Underpinning the General Ledger & Financial Reporting Cycle

Activities in the general ledger and financial reporting cycle are supported by these technologies:

ERP (Enterprise Resource Planning) – integrated software that records and manages many different types of transactions within a single integrated database, e.g. SAP, Oracle

Helps to monitor and reconcile cash transactions easily and allows for automatic bank reconciliations

Can compare statements by downloading them straight from the bank website

Benefits: reduced costs, improved access to financial information, increased productivity, improved data quality and validity and fluidity of shared information

Example of how XBRL is used to add meaning to text data:

Data and the General Ledger & Financial Reporting Cycle

Transactional data extracted from:

Subsidiary ledgers – Accounts receivable ledger and Accounts payable ledger

Payroll data store (contains details of salary and wage transactions)

General Ledger & Financial Reporting Cycle Business Decisions

|

|

|---|---|

|

|

General Ledger & Financial Reporting

Cycle Documentation

General Ledger & Financial Reporting

Cycle Documentation

General Ledger & Financial Reporting Cycle Activities & Related Risks and Controls

|

|

|||

|---|---|---|---|---|

|

|

|||

|

|

|

||

|

|

|||

|

|

|

||

|

||||

|

|

|

Measuring General Ledger & Financial Reporting Cycle Performance

A range of metrics (measure

used for a specific purpose) are used to monitor performance against

general ledger and financial reporting cycle objectives. Examples of

metrics/KPIs for this cycle objectives include:

A range of metrics (measure

used for a specific purpose) are used to monitor performance against

general ledger and financial reporting cycle objectives. Examples of

metrics/KPIs for this cycle objectives include:

|

|

|

Ethical theories (Perspectives)

Consequence-based – Utilitarianism, e.g. Trolley problem

Are moral decisions made based on the outcome or about the manner in which you achieve them?

|

|

|---|---|

|

|

Deontological Perspectives (Non-consequentialist Ethics)

This is an approach to ethics that judges the morality of an action based on the action’s adherence to a rule(s)

Deontologists look at rules and duties. This perspective focuses on the action to take and does not consider the consequences of the action

Teleological Perspective (Consequentialist Ethics)

Limitations of Utilitarianism (Consequence-based)

If the consequence is to our benefit – this is considered unethical.

Ethical Decision Making Model

Recognise an ethical issue (privacy issue, accuracy issue, property issue, accessibility issue)

Do I have sufficient information to make a decision?

Which individuals and/or groups have an important stake in the outcome?

Evaluate alternative actions

Which option best serves the community as a whole and not just some members? (the common goods approach)

Make a decision and test it – consider all approaches, which option best addresses the situation?

Act and reflect on the outcome of decisions

Ethics & Information Technology

PRIVACY ISSUES

This involves collecting, storing and disseminating information about individuals.

What information about one’s self or one’s associations must a person reveal to others, under what conditions and with what safeguards?

Information Privacy and Issues

|

|

|---|---|

|

Why is information privacy important? – Because it can lead to identity theft…

How to Maintain Information Privacy

Choose websites monitored by independent organisations

Avoid having cookies left on your machine

Visit sites anonymously

Use caution when requesting confirm email

Use separate email account from normal to protect information from your employer, sellers, and anyone using your computer

Use a VPN (virtual private network)

Using a non-descriptive email address (doesn’t include name), e.g. flyingbananas2023@gmail.com

ACCURACY ISSUES

This involves authenticity, fidelity and correctness of information that is collected and processed.

Who is responsible for authenticity, fidelity and accuracy of information?

Information Accuracy

Sources of Information Errors:

Errors in computer output can come from 2 primary sources:

PROPERTY ISSUES

What are the just and fair prices for its exchange?

How should we handle software piracy (copying copyrighted software)?

How should experts who contribute their knowledge to create expert systems be compensated?

E.g. Your last paper has been copied and handed in as if it were from another person. The computer game has been copied without the programmer receiving proper compensation for his/her effort.

Information Property

Internal use – used within organisation only

External use – can be sold to outside parties

ACCESSIBILITY ISSUES

Who is allowed to access information?

How much should companies charge for permitting access to information?

Information Accessibility

Employers – they can legally limit, monitor and access activities on company-owned computers or networks as long as policy has been distributed to employees

Case Study: San Bernardino Shooting and Apple

Ethical Issues for businesses with an AIS

CUSTOMER PROTECTION & PRIVACY

∆ Users of websites can be profiled without their knowledge

∆ The Web is being used more for marketing and selling products

Ethical Issues in E-Commerce and M-Commerce

Where did they go after?

Which IP (Internet address)?

Cookies

Risks of businesses increasing their reliance on technology

Number of cyber attacks are growing each year…

Motives Behind Cyber attacks:

Financial losses

Cybercrime

Cybercrime is often used interchangeably with terms such as: Computer crime, Computer-related crime, E-crime, High tech crime, Cyber fraud, Internet crime

∆ Audits, internal and external auditing including IT Audits

Easier way to protect yourself from cyber threats? – Have good passwords

Ethics in the Corporate Environment

TOPIC 12: CLOUD COMPUTING AND AIS

Definitions of Cloud Computing

∆ It runs on a shared data centre and you just need to plug in Gmail vs. Microsoft

∆ You don’t need servers or storage, technical team, upgrades – it can be up and running in a few days

Types of Cloud Services

Types of applications include development and testing, application platform, integration, database, general,

e.g. Google App Engine, Oracle, Palantir, WindowsAzure AppFabric (cloud companies)

Advantages and Disadvantages of Cloud Computing

Advantages of Cloud Computing - Why is everyone choosing cloud computing?

Lower total cost of owning (cheaper)

Secure storage management

Disadvantages of Cloud Computing

x Reliability on internet connection x Data security measures of provider x Quality of service

x Reliability of service provider

Easy deployment

Independent of devices

Characteristics of Cloud Environments

Multi-tenant – deliver shared services (your information is comingled with information of other companies) meaning one app is being used by multiple companies, everyone customises it for their specific needs

Per-usage based pricing model – only pay for what you need

Why do companies use it?

COST SAVINGS

Pay only for the apps you use

DEPLOYMENT SPEED (Spotify: download sign up pay you have access to the service – very quick)

SECURITY

Secure data centers

Automatic backups, cloud service companies back up data more often

Cloud Computing Challenges

∆ Cloud Security policy/procedure transparency

∆ CSP business viability

∆ Disaster recovery

Note: CSP – cloud service provider