Send checks the cashier and copy the cash prelist party

ACCT 513 Accounting for Information Systems

Workshop 4 – Problem Document

Instructions:

For workshop 1, complete the following problems for each chapter noted:

Chapter 12: 12.2 and 12.8; Chapter 13: 13.10; Chapter 14: 14.2 and Case 14-1

Using closed loop verification could help with this problem. For example, when the employee enters the account number the system could retrieve and display the account name so the employee can verify the correct account number had been entered (Romney & Steinbart, 2015). Additionally, including a portion of the company name with the account number for each client can help with batch posting because the system can verify the name matches after finding a match for the customer number prior to posting the sale. It is important to note that a validity check would not work for this specific problem because the account number entered exists; it just belongs to a different customer.

Making a credit sale to a customer who is already four months behind in making payments on his account.

To prevent this issue, having the proper segregation of duties is necessary. The same person that collects payments should not have the authorization to write off uncollectible accounts-one person should handle cash payments from customers and another should handle write-offs.

Billing customers for the quantity ordered when the quantity shipped was actually less due to back ordering of some items.

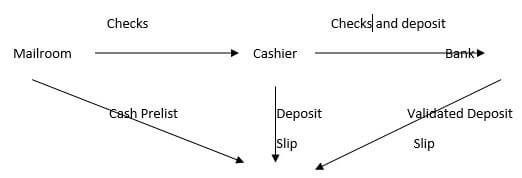

One way to prevent this issue is to have the mailroom create a cash prelist, send checks to the cashier and a copy of the cash prelist to a 3rd party. The cashier prepares a deposit slip for the checks-one goes to the bank with the check and one is sent to the 3rd party. The bank deposits the checks and send a validated deposit slip to the 3rd party. The 3rd party then compares the cash prelist, deposit slip, and validated deposit slip to be certain the cash received is the amount deposited.

Shipping goods to a customer but then failing to bill that customer.

To prevent this issue, segregating the shipping and billing functions is important. In addition, the system should be configured to compare sales orders, packing tickets, and shipping documents with sales invoices on a regular basis to determine if shipped items have been invoiced. For paper-based systems, pre-numbering all documents and periodically accounting for them identifies shipments that have not been invoiced (Romney & Steinbart, 2015).

Loss of all information about amounts owed by customers in New York City because the master database for that office was destroyed in a fire.

To prevent this issue, the company should do regular backups and store the most current off-site. In addition, having a cold or hot site and a well-developed disaster recovery plan is helpful.

A sales clerk sold a $7,000 wide-screen TV to a friend and altered the price to $700.

RFID tags and barcodes that automatically enter the pricing will help with this issue as would having a master list of prices and allowed discounts in the system. In addition, the sales clerk should not have authorization to change pricing unless it is approved by a manager and a log should be generated that shows the price changes, who approved them, and who rang them up.

12.8 Parktown Medical Center, Inc. is a small health care provider owned by a publicly held corporation. It employs seven salaried physicians, ten nurses, three support staff, and three clerical workers. The clerical workers perform such tasks as reception, correspondence, cash receipts, billing, and appointment scheduling. All are adequately bonded.

Most patients pay for services rendered by cash or check on the day of their visit. Sometimes, however, the physician who is to perform the respective services approves credit based on an interview. When credit is approved, the physician files a memo with one of the clerks to set up the receivable using data the physician generates.

Additional services are performed monthly by a local accountant who posts summaries prepared by the clerks to the general ledger, prepares income statements, and files the appropriate payroll forms and tax returns.

Required:

Control: Perform an external credit check to establish credit limits. This should be done by someone other than the doctor providing the service.

Weakness: The physician who approves credit also approves the write-off of uncollectible accounts.

Control: Segregation of duties where one person handles the cash receipt, one handles the billing, and still another maintains accounts receivable.

Weakness: The employee who makes bank deposits also reconciles bank statements.

Control: Segregation of duties where one employee makes the deposit and another issues credit memos.

Weakness: Trial balances of the accounts receivable subsidiary ledger are not prepared independently of, or verified and reconciled to, the accounts receivable control account in the general ledger.

Receiving The receiving department gets a copy of each purchase order. When equipment is received, that copy of the purchase order is stamped with the date and, if applicable, any differences between the quantity ordered and the quantity received are noted in red ink. The receiving clerk then forwards the stamped purchase order and equipment to the requisitioning department head and verbally notifies the purchasing department that the goods were received.

Accounts Payable Upon receipt of a purchase order, the accounts payable clerk files it in the open purchase order file. When a vendor invoice is received, it is matched with the applicable purchase order, and a payable is created by debiting the requisitioning department’s equipment account. Unpaid invoices are filed by due date. On the due date, a check is prepared and forwarded to the treasurer for signature. The invoice and purchase order are then filed by purchase order number in the paid invoice file.

The Weakness has been identified for you.

| Weakness | Control | Effect of new IT |

|---|---|---|

| 1. Buyer does not verify that the department head’s request is within budget. | Compare request to budget amount and against year to date figures. | IT would have an up to date amount remaining in the budget and can automatically compare the request against that amount. |

| 2. No procedures established to ensure the best price is obtained. | Get bids and quotes for orders, perhaps set a dollar amount or size requirement. | Internet or EDI can be used to get bids, |

| 3. Buyer does not check vendor’s past performance. | Vendor performance reports should be filled out and on suppliers and then reviewed when choosing a vendor. | Ratings on vendor performance are automatically updated and available to buyers at the click of a finger. |

| 4. Blind counts not made by receiving. | Purchase orders sent to receiving should have quantity ordered blacked out and having an incentive or reward program for employees that detect errors. | Receiving should be restricted from access to quantities ordered, bar coding or RFID tagging on purchase items with bar code readers and RFID scanners to check in purchases and incentives for detected discrepancies. |

| 5. Written notice of equipment receipt not sent to purchasing. | Written notice of equipment receipt is sent to purchasing. | Receiving info report entered into system on receiving terminal is sent or routed to purchasing. |

| 6. Written notice of equipment receipt not sent to accounts payable | Written notice is sent to accounts payable. | Program system to automatically send receiving report on equipment to accounts payable. |

| 7. Mathematical accuracy of vendor invoice is not verified. | Verify the accuracy of the math on the vendor invoice. | The math on the vendor invoice is automatically verified. |

| 8. Invoice quantity not compared to receiving report quantity. | Compare the quantity received on the receiving report with the quantity on the invoice to verify accuracy. | IT system automatically compares and verifies invoice quantity with receiving report quantity. |

| 9. Notification of acceptability of equipment from requesting department not obtained prior to recording payable. | Get confirmation from the requisitioner of acceptability of equipment order prior to recording payable. | Program system so it requires confirmation of acceptability of equipment before approval of invoice payment. |

| 10. Voucher package not sent to Treasurer. | Send voucher package to Treasurer . Should include supplier invoice and associated supporting documentation. | System is programmed to automatically correlate supplier invoice with supporting documentation. |

| 11. Voucher package not cancelled when invoice paid. | Voucher package marked paid when check is signed. | Program the system to cancel or mark all documents in the voucher package as paid when check is signed or payment made electronically. |

| 12. No mention of bank reconciliation. | Consistent bank reconciliation by someone that did not participate in either cash collections or disbursements. | Consistent bank reconciliation by someone that did not participate in either cash collections or disbursements. |

14.2 What internal control procedure(s) would best prevent or detect the following problems?

Inventory levels of finished goods

Inventory level of goods under production

Proper supervision by production supervisors

Have employees sign on the amount released and the amount received for work in process transfers

Monitor progress on rush orders

A production employee entered a materials requisition form into the system in order to steal $300 worth of parts from the raw materials storeroom.

Incorporate a limit check to validate the quantity entered against a fixed value like time scheduled or expected for the job

Incorporate programming so that if the data entered is not acceptable it prompts the worker to re-enter until it is

The discrepancy should show up in an unfavorable materials usage variance, since the shortage will necessitate requesting additional goods. To deter this type of problem:

Have the recipient of the materials sign for the quantity received

Restrict authority for expensive machinery to executive management

Accurately record/document the entire acquisition and disposal processes

A factory supervisor accessed the operations list file and inflated the standards for work completed in his department. Consequently, future performance reports show favorable budget variances for that department.

Log all changes to operations list file and review data in a timely way

Accurately record/document the entire asset disposal process

Require assets for write off be authorized by two managers

Examine issues of the Journal of Accountancy, Strategic Finance, and other business magazines for the past three years to find stories about current developments in factory automation. Write a brief report that discusses the accounting implications of one development: how it affects the efficiency and accuracy of data collection and any new opportunities for improving the quality of performance reports. Also discuss how the development affects the risks of various production cycle threats and the control procedures used to mitigate those risks.

Task requirements:

Answer below:

Ford Motor Company has developed IntoSite to help address the difficulties of sharing best practices across sites and fostering communication between widely dispersed manufacturing centers (Greenfield, 2014). IntoSite is “a software-as-a service application that uses a cloud-based web application using the Google Earth infrastructure to provide virtual navigation within Ford’s assembly plants” (Greenfield, para. 2). The site, accessible via a web browser, holds 2D and 3D versions of Ford’s assembly plants and allows users to obtain a better understanding of processes by navigating virtually through the plant and workstations (Greenfield). Not only can the user view a video but engineers can also add pins at specific spots to input relevant information on parts, processes, or key issues as well as provide simulations so workers see how to perform a job properly (Greenfield).

Romney, M & Steinbart, P. (2015). Accounting information systems (13th ed.). Upper Saddle

River, NJ: Pearson Education, Inc.