Accounts Receivable audit Assignment

The purpose of an Accounts Receivable audit is to ensure completeness and accuracy of the data and investigate for any potential risks that can be addressed by IDEA. Using IDEA improves the quality of audit and efficiency. The main purpose of an Accounts Receivable audit is to check if the debts that company has are valid. For accuracy, all files during the audit were totaled. The data analysis tools used for the audit were aged data analysis, identifying old invoices, credit balances, customers exceeding credit limit and unusually high value of debts.

AUDIT FINDINGS:

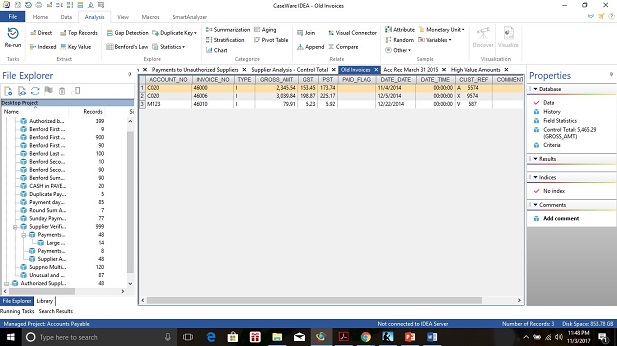

- The profile of accounts shows that most debt is current and there is only $5,465.29 from invoices which are more than 3 months old. Below is a screenshot of Old Invoices.

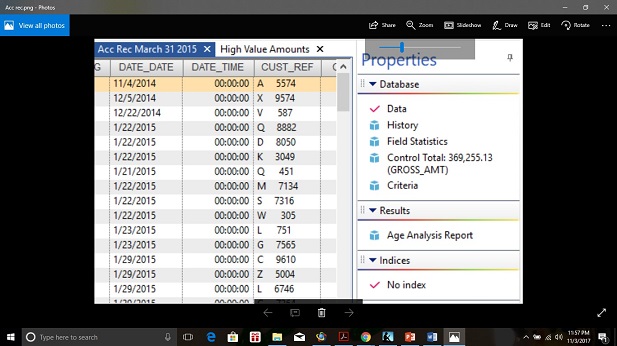

{" "} Ten items represent more than 38% of the total debt. The screenshots of the files ‘Acc Rec March 2015’ and ‘High value amounts’ respectively, show that 10 high value items have a debt of $139,479.86 which is 38% of the total debt $369,255.13. So, the company should focus on collecting from these high value accounts because that is a significant part of their debt.

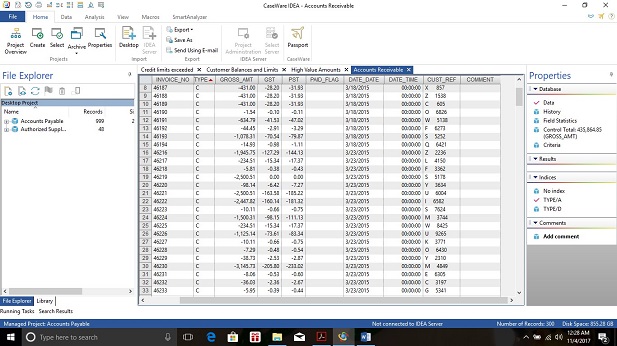

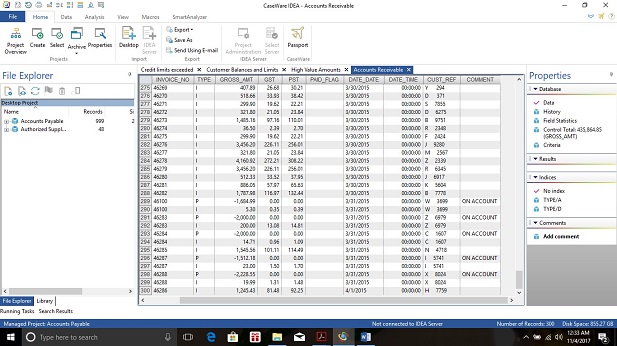

2. There are a significant number of credit items and payments received which were unallocated. The screenshot below shows Accounts Receivable file in which Credit sales are all ordered at the top and they represent a significant number in the list. The company needs to keep better records and no payments should be unallocated.

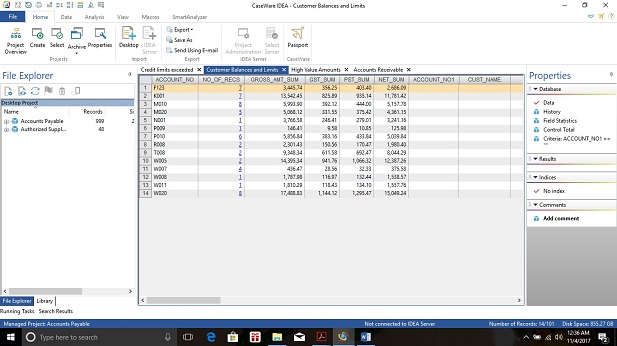

3. Credit has been given to 14 customers without being authorized as shown by the ‘Customer Balances and Limits’ file. It should be investigated as to why credit was extended to these customers without authorization.

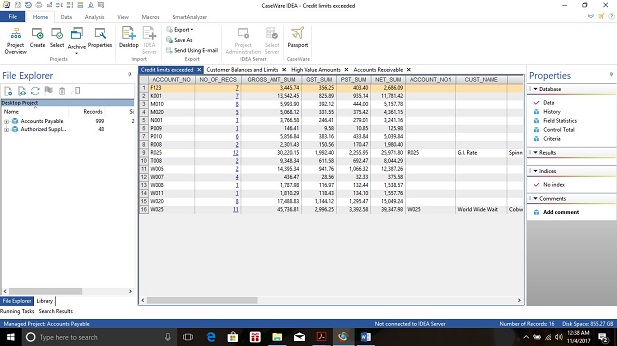

And ‘Credit Limits Exceeded’ table shows the two customers along with their names and addresses, who have exceeded the credit limit. If the company is unbale to collect from these customers, it should be written off as bad debt expense.

Topics in database

- Authorization: SQL Recursion

- Big Data

- Database and data science techniques

- Database Languages Assignment Help{" "}

- Database Design Help

- Database System Architectures Design

- Entity Relationship Model Understanding

- Higher-Level Design: UML Diagram Help

- Implementation Of Atomicity And Durability{" "}

- Object-Based Databases Homework Help

- Oracle 10g/11g

- Parallel And Distributed Databases

- Query Optimization Technique{" "}

- {" "} Relational Databases Homework Help

- Serializability And Recoverability

- SQL Join

- SQL Queries And Updates

- XML And Relational Algebra Homework Help

- XML Queries And Transformations

- Data Mining